How Stripe Tricked Me Into Paying More — And Wouldn't Let Me Undo It

Stripe sent me a one-click email to enable faster SEPA settlement. I clicked. Then a second email arrived with the fee they hadn't mentioned. When I tried to undo it, support told me I had to wait until the next day. Here's exactly what happened.

My business has been a Stripe customer for years. That's exactly why what happened this week left me genuinely frustrated. This is not a rage post. It's a detailed breakdown of a dark pattern — implemented by a company that should know better.

The email

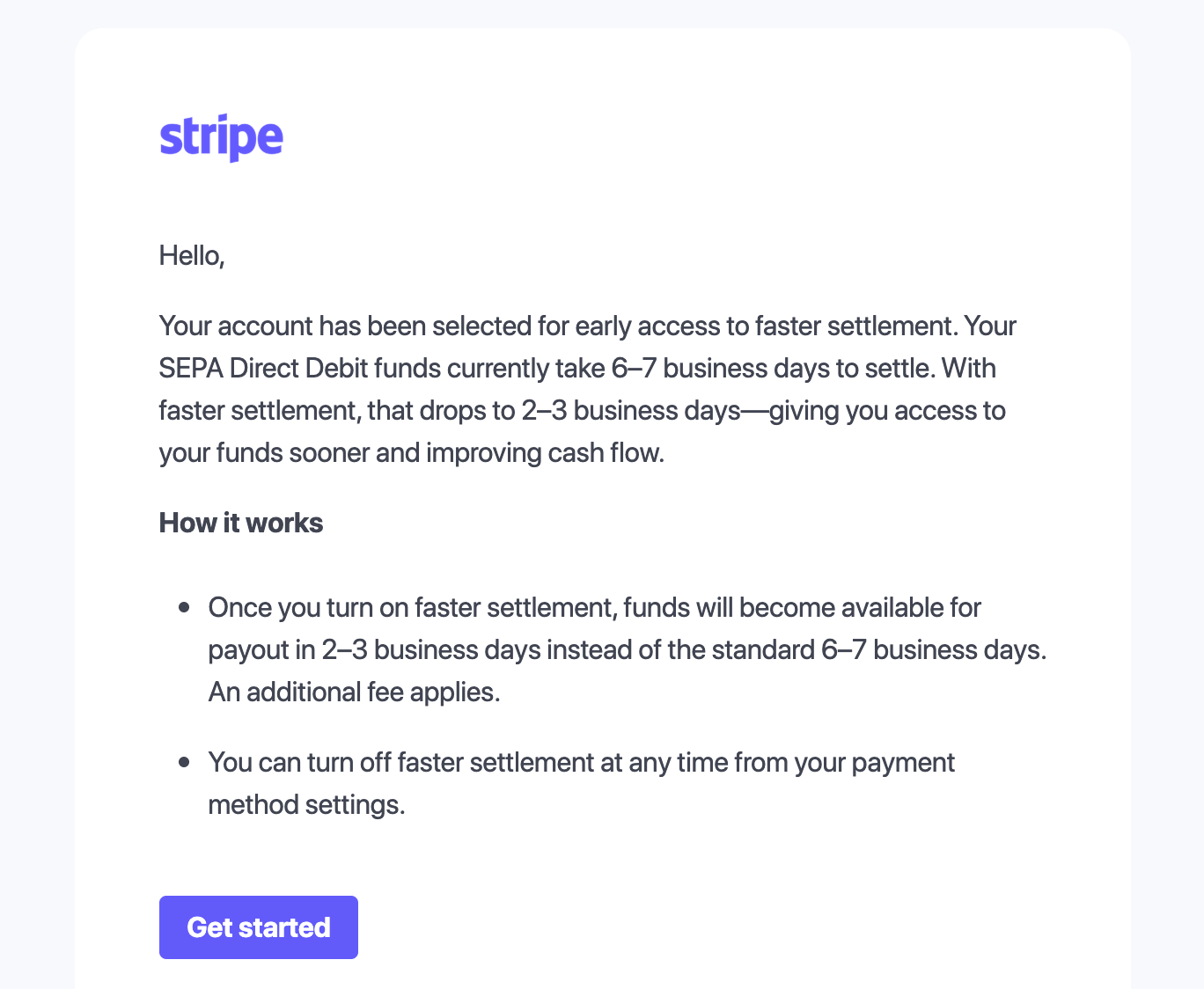

Today I received an email from Stripe. The subject line offered "early access to faster settlement" for SEPA Direct Debit. The copy was clean, warm, and benefit-forward:

Your funds currently take 6–7 business days to settle. With faster settlement, that drops to 2–3 business days — giving you access to your funds sooner and improving cash flow.

Who wouldn't want that? For any SaaS business that processes SEPA payments, 4 fewer days of float is genuinely useful.

Then came the "How it works" section. Two bullet points. The first led with the benefit — 2-3 business days instead of 6-7 — and then, tucked at the very end of that same bullet point, four words:

"An additional fee applies."

No amount. No percentage. No example calculation. No link to a pricing page. My brain didn't even register it.

The second bullet point immediately reassured me: "You can turn off faster settlement at any time from your payment method settings."

Then a big purple button. "Get started.". So I clicked it.

What happened next

One click. No confirmation screen. No "here is what this will cost you before you confirm." The feature activated immediately.

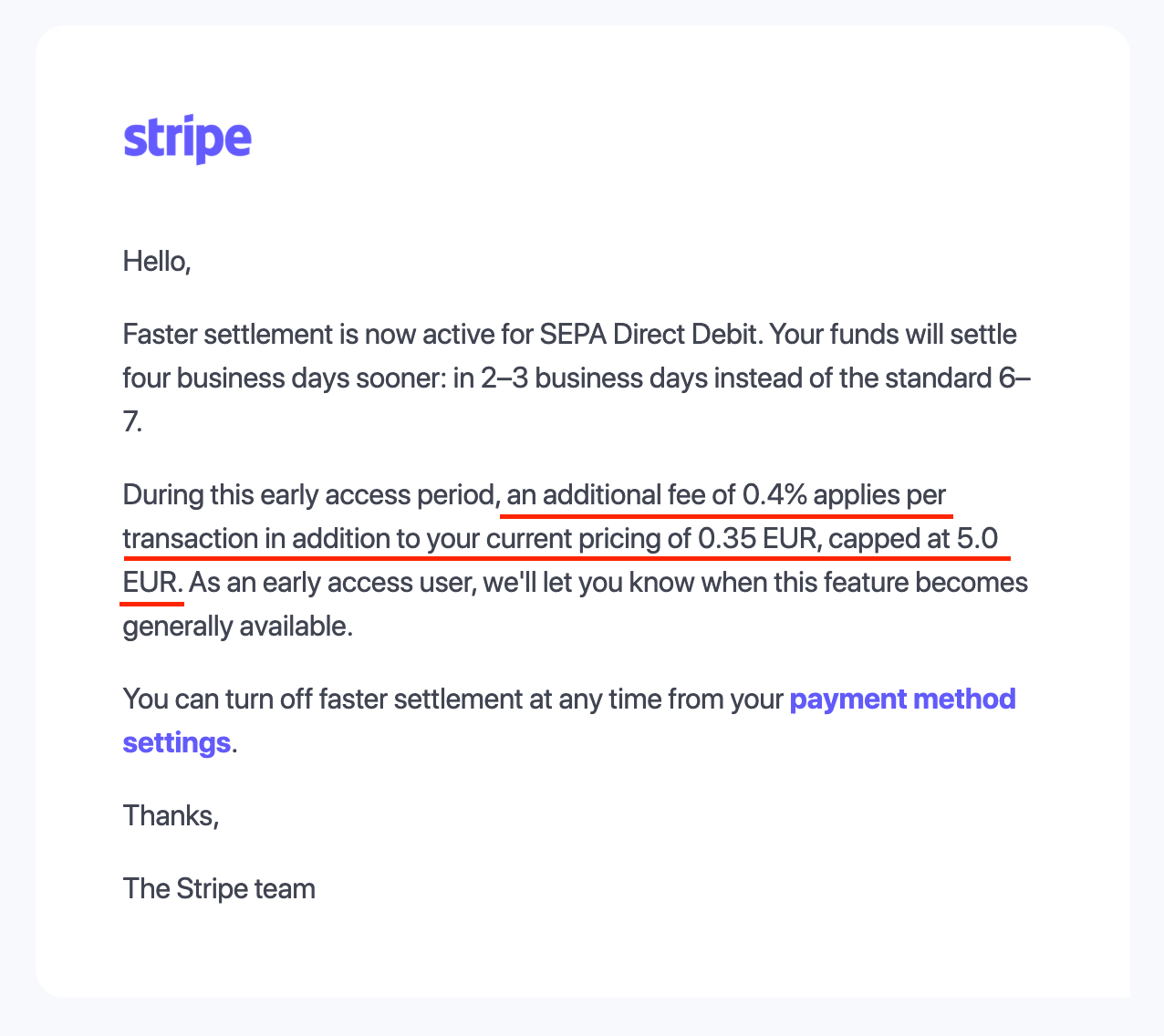

Seconds later, a second email arrived:

"Faster settlement is now active. An additional fee of 0.4% applies per transaction, in addition to your current pricing of 0.35 EUR, capped at 5.0 EUR."

0.4% per transaction. For a business processing significant SEPA Direct Debit volume, that is not a footnote. That is a material cost increase, activated without ever being shown the number before clicking confirm.

Then it got worse

The email said I could turn it off "at any time from your payment method settings." I immediately went to do exactly that.

The link in the email led me to a settings page where the toggle was nowhere to be found. I contacted Stripe support. Their answer: I could not disable it until the following day, when it would take effect.

They activated a new recurring fee on my account — without disclosing the amount before I confirmed — and when I tried to undo it immediately, I was told to come back tomorrow and do it myself.

"You can turn off faster settlement at any time" apparently means "you can turn it off, just not right now, after you've already enabled it by mistake."

Why this is a dark pattern

Let me be precise about what Stripe did here, because "dark pattern" gets thrown around loosely and I want to be specific.

The copy is engineered to maximise activation and minimise informed decision-making. The benefit is front and centre, repeated three times across the email. The fee is mentioned once, in four vague words, buried inside a bullet point that leads with something else entirely. There is no dollar amount, no percentage, no example of what a typical business would actually pay.

The activation flow has no friction by design. No confirmation screen. No "you are about to enable a 0.4% fee on all future SEPA transactions — confirm?" Just a single large CTA that goes straight to activation.

The opt-out reassurance is placed immediately after the fee mention, lowering your guard before you reach the button. "You can turn it off any time" is technically true — just not immediately true, as it turns out.

Each of these decisions individually might be defensible. Together, they form a pattern. The pattern is: get the customer to click before they've processed what it costs.

What Stripe should have done

This is genuinely not hard. The email should have said: "An additional fee of 0.4% per transaction applies." One sentence. The activation screen should have shown the fee, with an example — "for a €100 transaction, you would pay an additional €0.40" — before asking for confirmation. The opt-out should have been immediate, not deferred to the following day.

None of this is rocket science. Stripe knows how to build a clear confirmation flow. The fact that they chose not to here is a decision, not an oversight.

Why I'm writing this

Not to cancel Stripe. My company is still a customer and it'll probably remain one because there are sadly not much better alternatives that I know of. But I have a blog and a platform, and I think naming specific dark patterns when they happen — even from companies you respect — is more useful than silence.

If you use Stripe and process SEPA Direct Debit, check your payment method settings. If faster settlement is active on your account and you didn't consciously choose to pay 0.4% more per transaction, you may want to –try to– turn it off.

Comments ()