Before you tap 'Turn on Interest' in Wise, read this

Wise is marketing an investment product to millions of users with the aesthetics of a bank feature and no visible risk warnings. Their own data shows it lost money twice in five years. We've seen this before. It didn't end well.

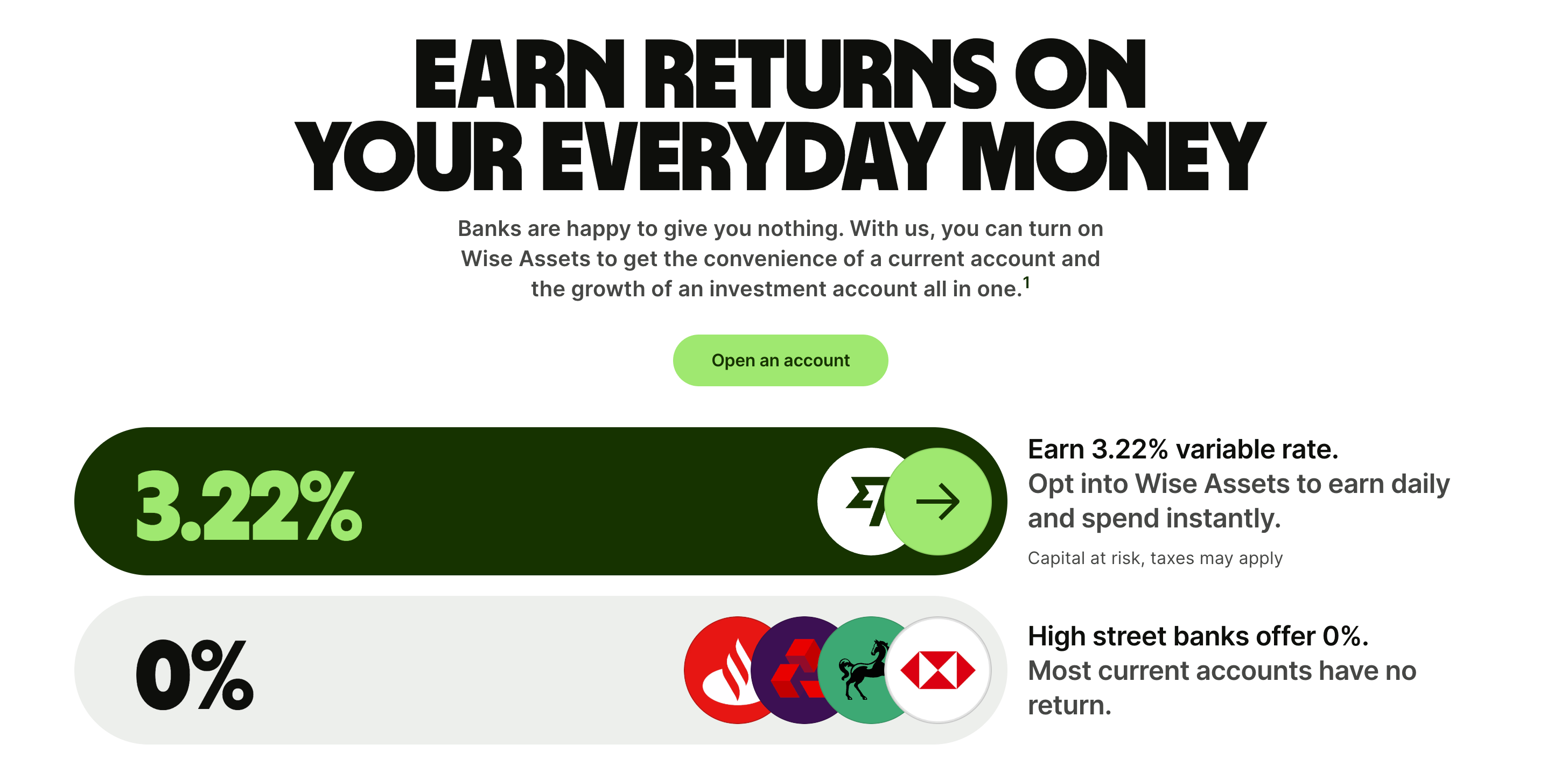

Wise is promoting its Interest feature everywhere right now. The pitch is simple and seductive: your money sits in your Wise account anyway — why not make it work for you? A tap of a button, 1.80% on your euros, no commitment, no lock-in. A green button. A growing plant. "Time to get growing."

It sounds innocuous. It sounds like a no-brainer. It sounds, frankly, like free money.

It isn't. And the way Wise is selling this is, in my view, genuinely irresponsible — because it follows a pattern that European consumers have seen before, have paid for before, and have spent decades trying to recover from.

Let me explain.

What Wise Interest actually is

When you activate Wise Interest, your money doesn't stay in your account in any meaningful sense. It is moved out of an e-money account — a protected cash balance — and invested in a fund: specifically, the BlackRock ICS Euro Government Liquidity Fund. Your balance is no longer your money sitting somewhere safe. It is a participation in an investment fund that tracks short-term government securities.

That fund can lose value. It has lost value. Wise's own historical data, published on their website, shows it plainly:

| Year | Fund return |

|---|---|

| 2021 | –0.7% |

| 2022 | –0.2% |

| 2023 | +3.1% |

| 2024 | +3.7% |

| 2025 | +2.2% |

In two of the last five years, customers who had activated Wise Interest lost money. Not theoretically. Not in a stress test scenario. Actually lost money, in normal market conditions, under ECB policy that was publicly known and widely discussed at the time.

Wise does acknowledge, in small print, that "growth is not guaranteed and your money is at risk if governments default or interest rates go negative." But that disclaimer is buried so far beneath layers of optimistic marketing language — "earn," "grow," "commitment-free" — that the overwhelming message a typical user receives is: this is safe, this is easy, this is basically free money.

It isn't any of those things. It is an investment. Investments carry risk. And selling an investment product to retail users with the aesthetics and emotional framing of a bank deposit feature is not new. We have a long, painful, expensive history of exactly this.

Spain: the preferentes scandal

In Spain, they were called participaciones preferentes — preference shares. Around 710,000 families were affected by products that were misleadingly presented as secure deposits. In total, €30 billion worth of these toxic products were issued since 1999. The typical buyers were pensioners who collectively bought around €30 billion of such shares. Rather than being warned of the inherent risks, they were reassured that these were safe options capable of yielding up to eight percent.

When the financial crisis hit, these investors found themselves forced to absorb almost €15 billion in losses. More than 103,000 lawsuits followed. The government had to intervene. Families lost savings accumulated over lifetimes.

In some cases, internal emails from bank branches actively encouraged staff to sell preference shares while explicitly lying about the conditions of these high-risk financial products.

The UK: Payment Protection Insurance

The PPI scandal is the most significant financial mis-selling scandal in United Kingdom history — globally, second in cost only to the mis-selling of residential mortgage-backed securities in the US before the 2008 financial crisis. Roughly 45 million policies were sold between 1990 and 2010. By 2021, total refunds paid to customers exceeded £38.3 billion.

PPI was sold alongside mortgages, credit cards, and personal loans — often without customers even knowing they had purchased it. Bonus schemes meant that advisers at some banks received six times as much commission for selling a loan with PPI attached as for selling a loan without it. The incentive to mis-sell was structurally embedded in how staff were paid.

Italy: subordinated bonds and the bail-in

Italy's version was arguably the most devastating at the individual level. Fitch Ratings estimated that one third of all investors in Italian bank bonds were retail investors. The December 2015 bail-in of investors in Banca Etruria led to the suicide of an Italian pensioner.

At Monte dei Paschi di Siena, around 40,000 small investors — most of whom had been steered by the bank into converting their deposits into bonds — faced losing approximately €2.2 billion. These were ordinary savers who walked into their local branch and trusted their banker. The Italian government ultimately had to invest an additional €1.5 billion specifically to compensate retail bondholders who had been determined to be victims of mis-selling.

The same pattern, every time

Across Spain, the UK, and Italy — and in variations across virtually every European country — the structure is always the same:

- A financial product that carries real risk

- Marketed to ordinary retail customers using the language and aesthetics of something safe and simple

- Risk disclosure buried, minimised, or absent

- Backed by aggressive commercial incentives

- Enabled by regulators who moved too slowly

- Followed by billions in compensation, eroded trust, and lasting damage to real people

The products were different. The mechanism was identical.

The regulatory questions Wise should be asked

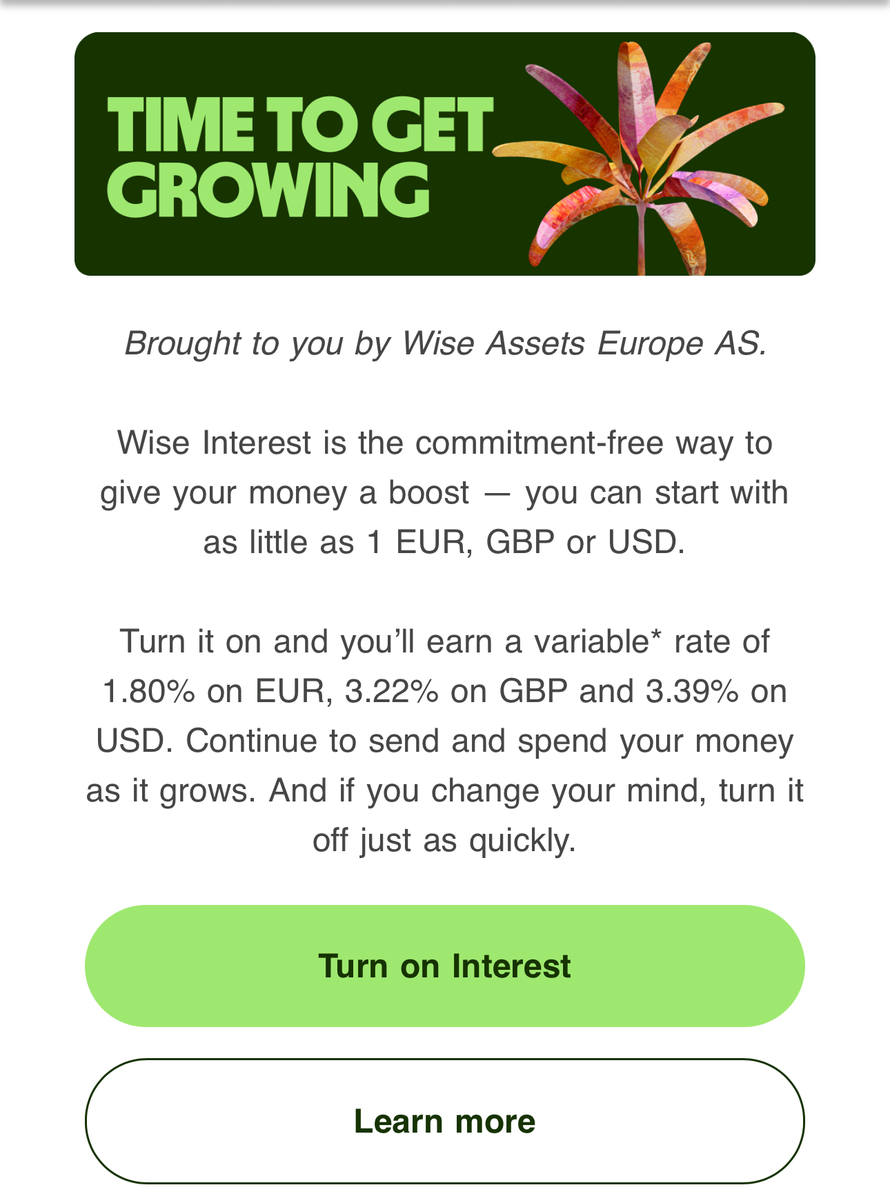

Wise isn't just putting this on a webpage buried under marketing copy. They are sending it directly to customers' inboxes. The email below is a real communication Wise pushed to its users.

Read it carefully: "Time to Get Growing." A brightly coloured plant. "Commitment-free." "You'll earn a variable rate." One large green button: Turn on Interest. That's it. No mention that your money leaves a protected cash account. No mention that the fund returned –0.7% in 2021 and –0.2% in 2022. No mention of investment risk in any language a normal person would notice.

A regulator reviewing this email under MiFID II fair communication standards could have serious questions to ask, such as:

1. Informed consent. Do users genuinely understand that activating "Interest" converts their cash balance into a fund participation with a different legal nature and a different risk profile? Or do they think they're turning on a savings feature?

2. MiFID II compliance. EU rules require that investment products be communicated in a way that is fair, clear, and not misleading. Does Wise's marketing — "Time to get growing," a green button, a flowering plant, the word "earn" used without qualification — meet that standard?

3. Suitability. MiFID II requires firms to assess whether a product is appropriate for the client. A blanket opt-in button on a consumer fintech app is not a suitability assessment. Who is verifying that Wise's 10+ million users are appropriate recipients of an investment product?

4. The nature of the change. A Wise e-money account and a Wise Interest account are fundamentally different things, with different protections and different risks. Is the transition between them being communicated clearly enough for a non-financial user to understand what they are agreeing to?

I want to be precise: Wise Interest is not a preference share. The BlackRock fund it uses is a legitimate, low-risk instrument. I am not accusing Wise of fraud.

What I am questioning is whether this product is being sold responsibly to the people who are actually buying it — ordinary users of a payments app who signed up to send money abroad, not to invest.

The bottom line

The history of financial mis-selling in Europe is not a history of outright fraud in most cases. It is a history of products that were technically legitimate, marketed in ways that obscured what they actually were, to people who were not equipped to evaluate the risks — and of regulators who took too long to act.

Before you tap that green button: you are not turning on a savings account. You are choosing to invest. In two of the last five years, that investment lost money. Make that choice with your eyes open — because Wise's marketing is doing its best to keep them half-closed.

Comments ()